Comparison of Old ITSA Forms to the New MTD IT Scheme

HM Revenue & Customs (HMRC) is phasing in Making Tax Digital for Income Tax (formerly known as MTD for ITSA), a fundamental shift designed to modernise tax filing. Quarterly digital updates and a final declaration are replacing the single annual submission. Although this shift simplifies the year-end tax filing workflow, it also brings new responsibilities for accountants and their clients.

In this guide, we will compare the old Self-Assessment process with the new MTD IT rules. You will see what’s different and what stays the same.

Who is Affected and When?

The transition to MTD for IT is being rolled out in phases, targeting self-employed individuals and landlords first. For accountants, this means that guiding clients through these changes will be a top priority.

- From April 2026: Mandatory for those with a total qualifying income over £50,000.

- From April 2027: Mandatory for those with a total qualifying income over £30,000.

Anyone below these thresholds, or with other types of income, will continue with the traditional Self-Assessment system for now.

The Traditional Self-Assessment

Currently, individuals file a self-assessment return annually using a set of HMRC forms. These forms covered income from various sources, including self-employment, property, employment, and others, all consolidated into a single return under different forms. The following forms are generally submitted to HMRC depending on the individual’s income sources.

| Form | Purpose |

|---|---|

| SA100 | Main individual tax return |

| SA101 | Additional income or claims (e.g. taxed interest, chargeable event gains) |

| SA102 | Employment income (e.g. wages, PAYE, benefits) |

| SA103 | Self-employment income |

| SA104 | Partnership income (individual partner’s share) |

| SA105 | UK property income |

| SA106 | Foreign income and gains |

| SA107 | Trust income |

| SA108 | Capital gains |

| SA109 | Non-residency and remittance basis cases |

| SA200 | Simplified return for straightforward tax affairs |

| SA800 | Partnership tax return (filed by the partnership) |

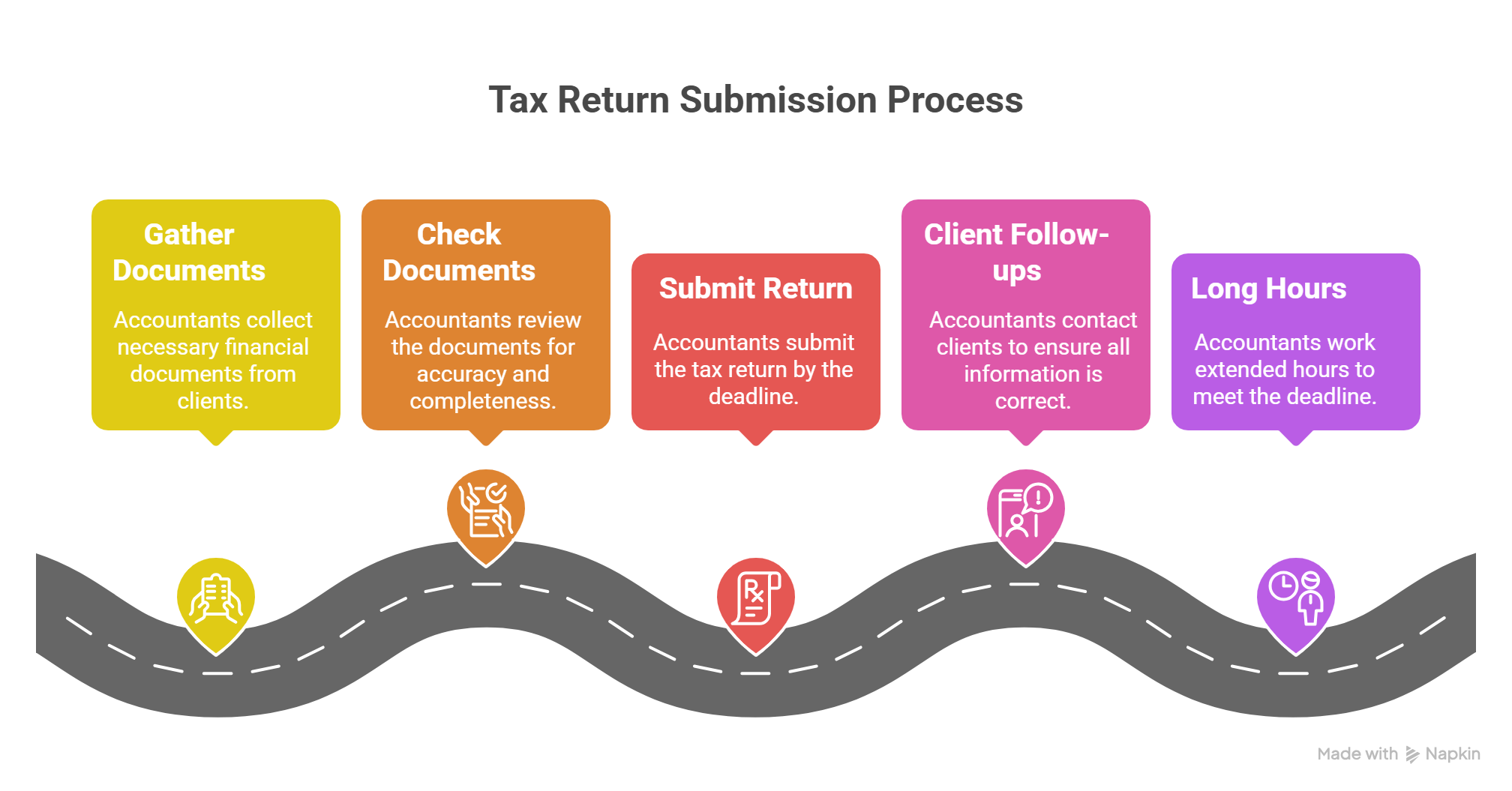

The return is usually submitted by 31 January at the end of the tax year. Since everything had to be gathered, checked, and submitted all at once, accountants faced a huge spike in workload as the deadline approached. For many firms, January is a period of intense client follow-ups and long hours to meet the submission deadline.

The New MTD for Income Tax Scheme

The new scheme replaces the traditional annual filing model with a multi-step digital process. Taxpayers are now required to provide data throughout the year using MTD-compatible software. This shift from paper to digital workflows moves the focus from reactive, once-a-year reporting to proactive and ongoing compliance. Here is how old self-assessment forms map to the new MTD stages:

| New MTD for ITSA Stage | Purpose | Replaces the old Forms |

|---|---|---|

| Quarterly Updates | Submit summaries of income and expenses every three months. | SA103 (Self-employment) SA105 (UK Property) |

| Final Declaration | A final submission that includes all other income, reliefs and allowances, and provides the final tax calculation for the year. | SA100, SA102, SA106, SA108 and SA101 |

The following is a summary of changes:

- Frequency: Moves from one annual tax return to four quarterly digital updates plus a final declaration.

- Format: Digital submission is now mandatory through approved software, replacing paper forms and the old HMRC portal.

- Structure: Splits the return into stages. Quarterly updates replace forms for self-employment (SA103) and property (SA105), while other income is handled in a final declaration.

- Who’s Affected: Initially mandatory for self-employed individuals and landlords with income over £50,000 (from 2026) and £30,000 (from 2027).

You can find more details about the new MTD Income Tax scheme in the following article: Understanding MTD IT for Self-Employed Business Owners.

Traditional Self-Assessment Is Still Required in Some Cases

MTD for IT has not yet replaced the entire Self-Assessment system. It currently only applies to individuals with self-employment or UK property income above the mandatory thresholds.

Here are some forms and taxpayer scenarios that are not included in the upcoming MTD for the ITSA mandate, and these individuals must file their self-assessment returns using the current process only:

The following forms are not yet supported under MTD and must still be filed using the existing Self-Assessment process:

- SA800 – Used by partnerships to file their tax return

- SA104 – Used by individual partners to report their share of partnership income

- SA107 – Used to report trust income

- SA109 – Used for non-residency, remittance basis, and other complex cases

- SA200 – A simplified return for individuals with straightforward tax affairs

Conclusion

MTD for ITSA is changing how accountants work with clients and HMRC. Instead of one big yearly deadline, firms now need to manage financial data continuously to meet quarterly submissions. To stay ahead, it’s essential to review your tech stack, categorise clients by income thresholds, and help them understand the changes to their record-keeping. Understanding the key challenges of MTD can help firms strategise effectively. This shift calls for more than just awareness; it requires automation tools like Receipt Bot to digitise the workflow.

Simplifying MTD IT with Receipt Bot

Receipt Bot is built specifically to support the demands of MTD. It captures, extracts, and categorises receipts, invoices, and bank statements. It also turns scattered documents into clean, structured, MTD-ready data that flows easily into your tax software.

Start your free trial today and simplify your workflow with Receipt Bot.